How to Cut €500 From Your Monthly Expenses Without Feeling It

You don't need to earn more money to have more money. In most households, $500 worth of invisible waste is already leaving every month spending so habitual and automatic that nobody even notices it's gone when it stops.

When most people think about cutting expenses, they picture sacrifice no more restaurants, no more coffee, no more anything enjoyable. That mental image is exactly why most people never start. It feels like punishment.

But the reality of where most household money actually leaks is far less dramatic. It's not the things you consciously enjoy. It's the things you're paying for without thinking subscriptions you forgot, habits you never chose, and inefficiencies that quietly drain $20, $30, $50 at a time until the total is genuinely shocking.

This guide finds that money. All of it without touching a single thing you'd actually miss.

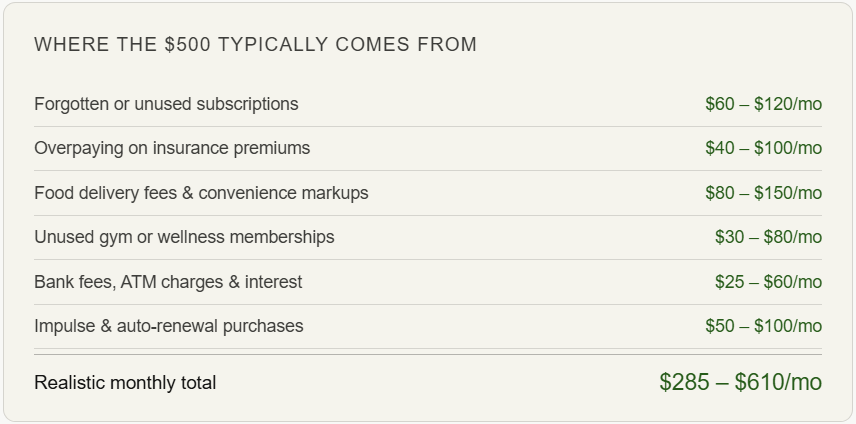

Where $500 typically hides in a monthly budget

Before making any cuts, it helps to see the total picture. Here's a realistic breakdown of where most households find their invisible $500:

None of those categories require giving up anything you actively value. They're all spending that happens on autopilot and autopilot is exactly where most financial waste lives.

Cut 1 - Subscriptions: the silent budget killer

📱 Audit every recurring charge this week

Save $60–$120/mo

Go through your bank and credit card statements line by line not mentally, actually in writing. The average household in 2026 pays for 12 or more subscriptions, but believes they have around 5. Streaming services, cloud storage duplicates, news apps, fitness apps, software trials that converted to paid, and free trials that weren't cancelled account for most of it. Cancel anything you haven't opened in the last 30 days without hesitation. You won't miss them you already weren't using them.

Do this in 10 minutes: Search your email inbox for the word "receipt" or "subscription." Every result is a recurring charge. Go through each one and decide: cancel or keep. Most people find at least 4–6 things they forgot they were paying for.

Cut 2 - Insurance: the bill nobody renegotiates

🛡️ Shop your car and home insurance annually

Save $40–$100/mo

Insurance companies count on loyalty. Staying with the same provider year after year almost always means paying more than a new customer would. Shopping your auto and home insurance once a year using comparison sites or calling 2–3 competitors typically saves $500–$1,200 annually for the exact same coverage. This is one of the highest-return, lowest-effort financial moves available, and most people never do it simply because it feels like a hassle. It takes about 20 minutes.

Also worth checking: If your car is older and fully paid off, you may be overinsured. Dropping comprehensive and collision coverage on a vehicle worth under $4,000 can save $50–$80 a month while making complete financial sense given the vehicle's actual value.

Cut 3 - Food spending: the category with the most invisible waste

🍔 Reduce delivery and convenience markups

Save $80–$150/mo

Food delivery apps are one of the most expensive habits in modern household budgets not because of the food itself, but the markup. A $14 meal at a restaurant costs $22–$28 delivered once fees, tips, and surge pricing are added. Two or three deliveries a week compounds to $250–$400 a month for a single person. Reducing delivery to once a week and batch-cooking two or three simple meals doesn't feel like deprivation it just shifts the habit slightly. The savings are immediate and significant.

🛒 Switch one grocery habit, not your whole routine

Save $30–$60/mo

Switching from name brands to store brands on 5–6 staple items (pasta, canned goods, dairy, cooking oil, cleaning supplies) typically saves 25–40% on those items with no meaningful quality difference. You don't need to change your entire shopping routine just make the switch on the things where the brand genuinely doesn't matter. Most people can't tell the difference in a blind taste test. Your bank account always can.

Cut 4 - Bank fees and interest: the most avoidable expenses

🏦 Eliminate monthly fees and minimum interest charges

Save $25–$60/mo

Monthly account maintenance fees, out-of-network ATM charges, and minimum credit card interest payments are pure waste money that buys you nothing. Switching to a fee-free online bank (Ally, Marcus, Chime) eliminates maintenance fees entirely. Paying your credit card balance in full each month, even if it's not the full amount you owe, eliminates new interest charges going forward. These changes cost nothing and have no lifestyle impact whatsoever.

Cut 5 - The impulse and auto-renewal trap

🔄 Add a 48-hour rule for non-essential purchases

Save $50–$100/mo

Impulse spending is not a willpower problem it's a system problem. The simplest system fix is a 48-hour waiting rule: anything non-essential goes into a cart or a notes app and waits 48 hours before you buy it. Research consistently shows that 60–70% of impulse purchases feel unnecessary two days later. You don't fight the urge you just delay it, and most of the time it disappears on its own. This one behavioral shift saves the average person $600–$1,200 a year.

Why "without feeling it" is the actual strategy

Most budgeting advice focuses on discipline spend less, resist more, sacrifice harder. That approach fails for the vast majority of people because it relies on willpower, which is finite and inconsistent.

The cuts in this guide work because they target spending you're already not getting value from. Cancelling a subscription you forgot about doesn't feel like deprivation it feels like finding money. Shopping your insurance doesn't change your coverage — it just reduces what you pay for it. Switching five grocery items to store brands doesn't change your meals it just costs less.

Myth - Cutting expenses means living with less and enjoying life less.

Reality - Most household spending waste is invisible automatic charges, forgotten memberships, and convenience markups on things you don't consciously value. Removing them changes your bank balance without changing your life.

What $500 a month actually becomes

Finding $500 a month in your current budget isn't just a short-term fix. Redirected consistently, that money changes your financial picture significantly over time.

At $500 a month invested in a basic index fund at 8% average annual return: after 5 years, you'd have roughly $36,000. After 10 years, $91,000. After 20 years, over $294,000. That money was already leaving your account every month it was just going to forgotten subscriptions, delivery fees, and bank charges instead of your future.

Start this weekend: Block 30 minutes. Open your bank statement. Search your email for "subscription." List every recurring charge. Cancel anything unused. That single session will likely save you $60–$120 this month with zero lifestyle change and give you a clear picture of where the rest of the $500 is hiding