Investing in Gold: Hedge Against Inflation or Overhyped?

Every time inflation rises, gold gets its moment in the spotlight. Financial commentators tout it as the ultimate safe haven, and ads for gold coins flood the internet. But is gold actually a reliable hedge against inflation or is it a compelling story that doesn't always hold up in practice? The answer is more nuanced than either side wants to admit.

Why Investors Have Trusted Gold for Centuries

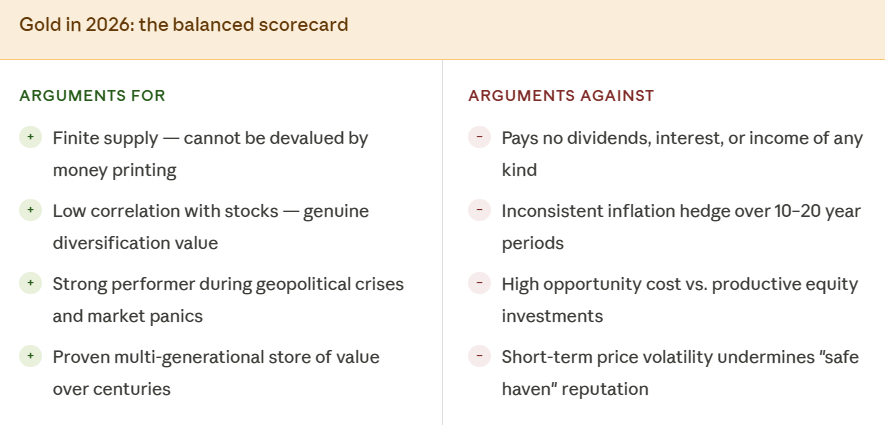

Gold's appeal is rooted in something simple: it can't be printed. Unlike paper currency, which governments can produce at will, the global supply of gold grows by only about 1–2% per year through mining. This finite supply is the core of gold's inflation-hedge argument when governments print money and currency loses purchasing power, gold is supposed to hold its value.

Historically, there is truth to this. Over very long time horizons decades and centuries gold has broadly maintained purchasing power. An ounce of gold bought roughly the same amount in ancient Rome as it does today, in terms of fine clothing or quality goods. As a multi-generational store of value, gold has a genuine track record.

Gold also behaves differently from stocks and bonds. When financial markets panic think 2008, 2020, or geopolitical crises investors often rotate into gold as a "flight to safety." This low correlation with equities is genuinely valuable for portfolio diversification, even if you're skeptical of the inflation narrative.

Where the Inflation-Hedge Argument Gets Complicated

Here's what gold advocates don't always mention: over medium-term periods, the relationship between gold prices and inflation is surprisingly inconsistent. During the high-inflation years of 2021–2022, for example, gold actually underperformed inflation-linked bonds and even some equity sectors. The "gold always beats inflation" narrative breaks down when you look at 10–20 year windows rather than century-long trends.

Gold also generates no income. It pays no dividends, no interest, no rent. A share of stock represents ownership in a business that produces goods, earns revenue, and can grow. A bond pays regular interest. Gold just sits there. This is why legendary investor Warren Buffett has long been skeptical of gold as a long-term wealth builder the opportunity cost of holding gold instead of productive assets is real.

The opportunity cost reality: $10,000 invested in a low-cost S&P 500 index fund in 2010 would be worth over $55,000 today. The same amount in gold would be worth significantly less and you'd have received zero income along the way.

There's also the storage and insurance problem. Physical gold requires secure storage and insurance, which adds ongoing costs that quietly erode your real returns. And gold prices can be volatile in the short term it's entirely possible to buy gold as an "inflation hedge" and watch it drop 15–20% over the following year.

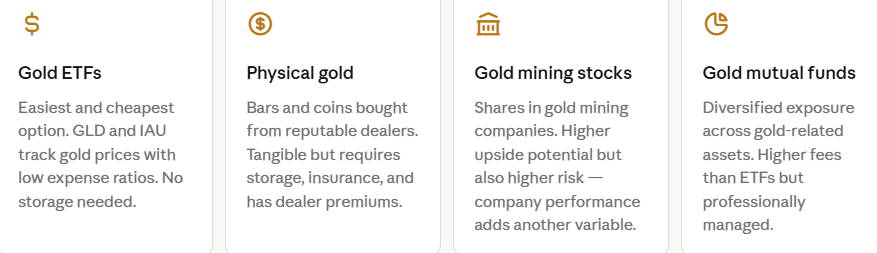

The Practical Ways to Add Gold to a Portfolio

If you've decided gold deserves a place in your portfolio, the method you choose matters significantly in terms of costs, taxes, and practicality.

For most retail investors, a gold ETF like IAU (iShares Gold Trust) is the simplest, lowest-cost, and most liquid way to gain gold exposure. The annual expense ratio is around 0.25% far cheaper than the ongoing costs of holding physical gold.

So - Should You Invest in Gold in 2026?

The answer depends on what you're trying to solve. If you're looking for a single investment to beat inflation year in and year out, gold will disappoint you more often than you'd expect. The data does not consistently support gold as a short-to-medium term inflation fighter.

However, as one component of a diversified portfolio typically 5–10% of total holdings gold serves a legitimate purpose. It tends to rise during financial crises, geopolitical instability, and dollar weakness. It adds a layer of protection that bonds and stocks don't always provide simultaneously. In that narrower role, gold earns its place.

The investors who get hurt by gold are the ones who go all-in on it, driven by fear or media hype, and discover that its short-term price is just as unpredictable as any other asset class. Used thoughtfully as a diversifier not as a core wealth-builder gold is a reasonable tool in the right hands.

The bottom line: gold isn't magic, and it isn't worthless. It's a specific tool that does specific things well and understanding that distinction is what separates thoughtful gold investors from those who buy at the top of a hype cycle and regret it six months later.