Why Your Credit Card Minimum Payment Is a Trap - And How to Escape It

The minimum payment isn't there to help you get out of debt. It's designed to keep you in it - for as long as possible, paying as much interest as possible. And until you see the math, it's almost impossible to believe how effective that design really is.

If you've ever looked at your credit card statement, seen the minimum payment amount, and thought "at least I'm staying on top of it" - this article is for you. Because what feels like responsible debt management is, in practice, one of the most expensive financial habits a person can have.

Credit card companies are not your financial partner. They are a business. And the minimum payment system is one of the most cleverly engineered features in modern personal finance built to maximize the amount of interest you pay while keeping you just comfortable enough not to panic.

Here's exactly how it works, what it costs you, and how to break out of it.

The number on your statement that looks small on purpose

Credit card minimum payments are typically calculated as either a flat amount (often $25–$35) or a small percentage of your outstanding balance usually 1–3%. That number is deliberately low. Not because the bank is being generous, but because the lower your minimum payment, the longer it takes to pay off the balance, and the more interest they collect.

The real cost of minimum payments on a $5,000 balance at 22% APR:

Paying only the minimum each month: approximately 17–19 years to pay off. Total interest paid: $6,300–$7,100 more than the original balance itself. You would pay for that $5,000 worth of purchases more than twice over.

That's not a worst-case scenario. That's the mathematical reality of a completely average credit card balance at a completely average interest rate in 2026. Most people carrying a balance have no idea this is happening to them.

How minimum payments are calculated - and why it matters

📊 Interest accrues daily, not monthly

Most people think interest is charged once a month. In reality, credit card interest accrues every single day based on your daily balance. Your annual percentage rate (APR) is divided by 365 to calculate a daily rate. On a $5,000 balance at 22% APR, that's roughly $3 in interest every single day whether you make a purchase or not. By the time your statement arrives, interest has already been compounding for 30 days.

💸 Most of your minimum payment goes to interest, not principal

On a $5,000 balance at 22% APR, the minimum payment might be around $100. Of that $100, approximately $90 goes toward interest and fees and only $10 reduces your actual balance. You've paid $100 and are now $10 less in debt. At that rate, paying off the balance feels impossible because it effectively is, unless you change something.

📉 The minimum payment shrinks as your balance decreases

Because minimum payments are calculated as a percentage of the outstanding balance, they get smaller as you pay down the debt. This sounds helpful but it means your payoff timeline stretches even further. A $100 minimum this month becomes $97 next month, then $94 the month after. The debt decreases in slow motion while interest keeps compounding at the same rate.

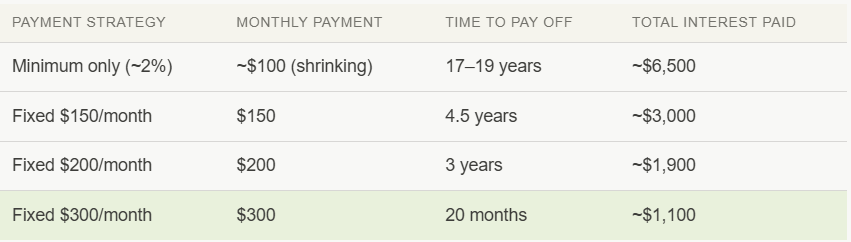

The comparison that changes everything

The most powerful way to understand the minimum payment trap is to compare it directly to the alternatives on the same balance.

Based on a $5,000 balance at 22% APR — a common scenario in 2026.

The difference between paying minimum only and paying $300 a month isn't just 15 years of your life. It's $5,400 in interest that goes directly into the bank's pocket instead of yours. That money could have been an emergency fund, a vacation, a down payment, or an investment growing quietly toward retirement.

Why the system is designed this way

This isn't accidental. Credit card companies earn more revenue when customers carry balances. A cardholder who pays their full balance every month generates very little profit for the bank only merchant processing fees. A cardholder who pays the minimum on a $5,000 balance generates thousands of dollars in interest over the life of that debt.

What credit card statements are legally required to show in the US: Since 2010, the CARD Act has required statements to show a "minimum payment warning" telling you exactly how long it will take to pay off your balance paying only the minimum, and what you'd need to pay monthly to clear it in 3 years. Most people scroll past it. It's one of the most important numbers on the entire statement.

The minimum payment also serves a psychological purpose. It signals "you're handling this" removing the urgency to aggressively pay down the balance. Comfort is the enemy of debt payoff. The minimum payment is designed to keep you comfortable while the interest clock runs.

The three warning signs you're deeper in the trap than you realize

Warning Your balance isn't going down month to month. If you're making minimum payments but also using the card for regular purchases, your balance may be growing even while you pay. Interest and new charges can easily outpace a minimum payment, meaning you're moving backward without realizing it.

Warning You have multiple cards with balances. Each card's minimum payment is calculated separately. Someone with three cards carrying balances may be paying $250+ per month in minimums while making almost no progress on any of them because the vast majority is going to interest across all three.

Warning You've been "managing" the same balance for over a year. If a credit card balance has been roughly the same for 12 months or more, minimum-only payments are likely keeping it afloat not reducing it. The interest charges are consuming your payments before they can dent the principal.

How to escape the minimum payment trap

- Pick a fixed amount - not a percentage - and commit to it

Set a specific dollar amount above the minimum and treat it like a bill. Even $50 above the minimum payment makes a significant difference in time and total interest. The key is keeping it fixed not letting it drift down with the balance. Automatic payments at a fixed amount are the simplest way to enforce this.

- Target the highest-interest card first (avalanche method)

If you have multiple cards with balances, pay minimums on all of them but put every extra dollar toward the card with the highest APR. Once that card is cleared, roll that payment into the next highest. This approach minimizes total interest paid and is mathematically the fastest path to being debt-free.

- Look into a 0% balance transfer card

Many credit cards offer 0% APR on balance transfers for 12–21 months. Moving a high-interest balance to one of these cards means every payment goes directly to reducing principal not feeding interest. This can cut years off your payoff timeline. The critical rule: don't accumulate new debt while paying off the transferred balance, and have a plan to pay it off before the promotional rate expires.

- Stop using the card while paying it off

It sounds obvious, but adding new purchases to a card you're trying to pay down is like bailing out a boat while leaving the tap on. Even small ongoing charges reset the compounding clock on your balance. Pay with debit or cash while in payoff mode even for just 3–6 months and the difference in progress is dramatic.

The bottom line

The minimum payment is not a safe floor. It's a treadmill designed to keep you moving without getting anywhere. Understanding this is the first step to changing it.

You don't need a dramatic financial overhaul to escape it. You need one decision: pay more than the minimum, every month, on a fixed schedule, until the balance is gone. The math then works for you instead of against you and the difference in what that choice saves over time is not small.

Do this right now: Open your most recent credit card statement. Find the "minimum payment warning" section the one that shows how long payoff takes at minimum only. Read that number. Then calculate what you'd need to pay monthly to clear it in 24 months instead. That gap is your target.